Disclaimer: The opinions expressed by our writers are their own and do not represent the views of U.Today. The financial and market information provided on U.Today is intended for informational purposes only. U.Today is not liable for any financial losses incurred while trading cryptocurrencies. Conduct your own research by contacting financial experts before making any investment decisions. We believe that all content is accurate as of the date of publication, but certain offers mentioned may no longer be available.

- Breakdown by Key Asset Categories (as of June 2025):

- RWA Infrastructure: Issuance, Compliance, and Settlement

- Ethereum as the Institutional Settlement Layer

- Regulatory Tailwinds: Catalyzing Institutional RWA Adoption

- Challenges and Strategic Outlook

- 2. Custodial Centralization Risks

- Outlook: Infrastructure First, Assets Next

- Conclusion: Laying the Rails for Onchain Capital Markets

- About CoinEx

Real World Asset (RWA) tokenization is a critical driver of institutional adoption and the broader convergence of traditional finance (TradFi) and decentralized finance (DeFi).By June 2025, RWA-related protocols have locked $12.7 billion in value, with tokenized U.S. Treasuries and private credit leading rapid growth under clearer regulatory frameworks and evolving on-chain infrastructure.

CoinEx Research believes RWAs are evolving from early-stage experimentation to institutional adoption — signaling the arrival of the on-chain asset era. This report shares CoinEx Research’s insights on the RWA landscape in two parts: Part I examines the foundational enablers of the on-chain asset era, while Part II shifts focus to the application layer—analyzing tokenized asset classes such as Treasuries, credit, stocks, bonds, and commodities, alongside key players and product structures driving growth.

Market Landscape: From Stablecoins to Treasuries-RWA, Market Is Concentrated but Accelerating

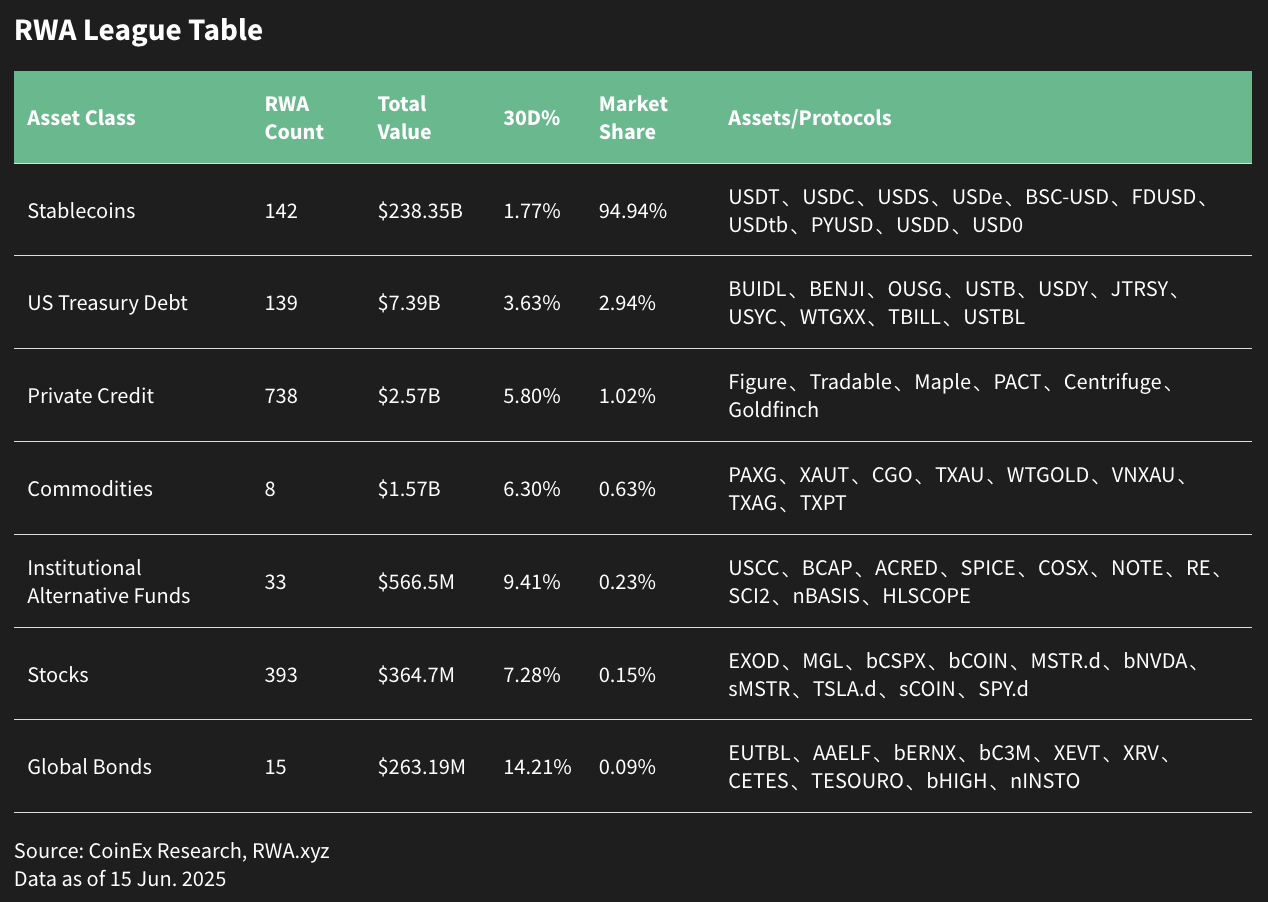

Real World Assets (RWAs) span a diverse set of tokenized off-chain assets—including stablecoins, U.S. Treasuries, commodities, private credit, equities, and bonds. According to the World Economic Forum, tokenized assets could eventually reach a total addressable market in the hundreds of trillions. As of June 2025, RWA-related protocols have locked $12.7B in value, growing 69% year-to-date and 282% year-over-year.

Despite this expansion, the market remains highly concentrated: stablecoins account for 94.9% of total RWA market cap ($238.3B), followed by Treasuries at 2.94% ($7.3B) and commodities at 0.63% ($1.5B). The rise of tokenized Treasuries—led by institutional issuers like BlackRock and Franklin Templeton—has driven much of this growth, with BlackRock’s BUIDL fund alone reaching $2.5B TVL and 44% market share in this segment.

Breakdown by Key Asset Categories (as of June 2025):

- Stablecoins ($238.3B, + dominance): Fiat-pegged tokens are foundational to on-chain liquidity and settlements; daily volume surpasses PayPal.

- Tokenized Treasuries ($7.3B, +933% YoY): Fastest-growing segment, enabled by Reg D/S issuers like BlackRock (BUIDL) and Franklin (BENJI).

- Private Credit ($2.57B, +5.8% MoM): High-yield debt for DAOs and funds; Maple Finance leads with 67% of active loans.

- Tokenized Commodities ($1.57B): Dominated by gold/silver tokens (PAXG, XAUT) used as collateral in DeFi.

- Alternative Funds ($567M): Tokenized hedge-like products for institutional allocators.

- Tokenized Equities ($365M, -7.2% MoM): Global retail access to stocks via platforms like Backed and Swarm.

- Non-U.S. Sovereign Bonds ($237M): Eurozone and Swiss pilots signal early adoption.

- Corporate Bonds ($16M): Still niche but structurally feasible under regulatory frameworks.

As institutional players explore new RWA types beyond stablecoins, regulatory clarity is emerging as a critical enabler for further adoption—especially in yield-bearing assets like Treasuries and private credit.

RWA Infrastructure: Issuance, Compliance, and Settlement

Tokenization Stack:From Legal Structuring to On-Chain Trading

The tokenization of real-world assets (RWAs) brings traditional financial instruments into programmable blockchain ecosystems. This process is not purely technical—it is deeply rooted in legal, custodial, and compliance infrastructure. A robust RWA issuance pipeline relies on five key layers.

1. Legal Foundations: Real Assets, Real Compliance

Every RWA token starts off-chain. The foundation is built through regulated intermediaries that mirror traditional financial workflows. Special Purpose Vehicles (SPVs) isolate legal ownership and ring-fence liability, while licensed asset managers structure the portfolios. Custodians—like BNY Mellon or CACEIS—hold the underlying Treasuries, bonds, or commodities.

BlackRock’s BUIDL and Franklin Templeton’s BENJI exemplify this architecture. Both are backed by regulated U.S. money market funds, issued via Securitize under SEC oversight. These tokens are not synthetic—they are on-chain mirrors of legally held and audited assets.

2. Verification and Valuation: Trust Anchored by Oracles

To maintain token credibility, the underlying assets must be regularly verified. Treasury-backed tokens rely on custodial proofs and attestations of reserve. For subjective assets like real estate or intellectual property, third-party appraisals and legal documentation are mandatory.

Oracles such as Chainlink serve as the critical middleware, offering proof-of-reserve, price feeds, and real-time attestations. They ensure consistency between off-chain asset status and on-chain token state—turning oracles into essential trust infrastructure.

Once verified, tokens are issued using standard smart contracts—most commonly ERC-20 for fungible assets. Ethereum remains the dominant issuance layer, with Base, Polygon, and Stellar following in volume. However, token standards alone are not sufficient.

Institutional RWA tokens incorporate transfer restrictions at the contract level. Permissions such as whitelisting, geofencing, and investor classification are enforced via platforms like Securitize. BUIDL, for example, is deployed across chains but enforces strict transfer logic through embedded compliance modules.

4.Compliance & Identity: KYC/AML and Access Control

To align with regulatory frameworks like the EU’s MiCA and the U.S. GENIUS Act, issuers integrate KYC and AML workflows. Platforms such as Securitize ID and Tokeny handle identity verification, while emerging zero-knowledge (ZK) solutions offer privacy-preserving compliance.

Token access is limited to verified wallets, and transactions are often restricted to specific jurisdictions or investor classes. These identity constraints are not optional—they are core infrastructure within the tokenization stack.

5.Trading & Redemption: Automated Compliance in Code

Tokens can be subscribed to with fiat or USDC, and are minted directly to compliant addresses. On the secondary market, transfers occur through DEXs or permissioned venues—though every trade must comply with embedded jurisdictional logic.

Smart contracts go beyond enabling transfers—they enforce eligibility, redemption throttling, and even time-locked access depending on regulatory context. In essence, compliance becomes code.

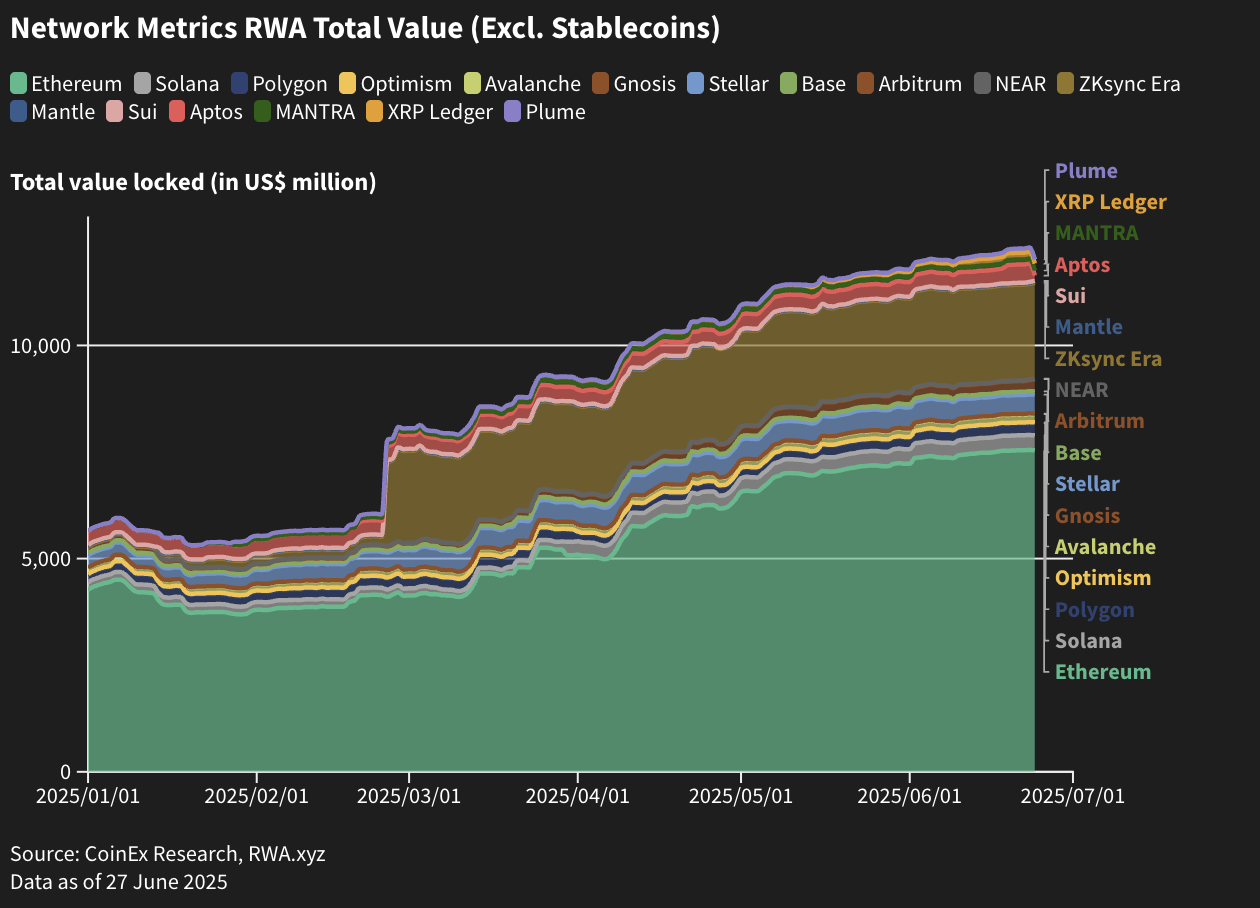

Ethereum as the Institutional Settlement Layer

Ethereum has become the institutional anchor for tokenized RWAs. Since early 2024, Ethereum has captured a growing share of non-stablecoin RWA activity—now accounting for over 59% of total TVL in this segment.

This dominance has been driven by the composability and maturity of Ethereum’s infrastructure. BlackRock’s BUIDL fund, with $2.7B in assets under management, allocates 93% of its supply to Ethereum. The network supports deep integrations with DeFi protocols like Aave and Uniswap, as well as institutional compliance layers such as Securitize and Chainlink.

This dominance has been driven by the composability and maturity of Ethereum’s infrastructure. BlackRock’s BUIDL fund, with $2.7B in assets under management, allocates 93% of its supply to Ethereum. The network supports deep integrations with DeFi protocols like Aave and Uniswap, as well as institutional compliance layers such as Securitize and Chainlink.

Ethereum’s RWA composition is also highly institutional: approximately 76% of tokenized RWAs on Ethereum are Treasuries, while around 20% are commodity-backed tokens such as PAXG. Other chains—zkSync, Stellar, and Base—host RWA deployments as well, but often face ecosystem fragmentation and over-reliance on a single issuer or product line.

As RWAs move from pilot to scale, Ethereum remains the settlement layer of choice—driven by trust, composability, and regulatory-aligned infrastructure.

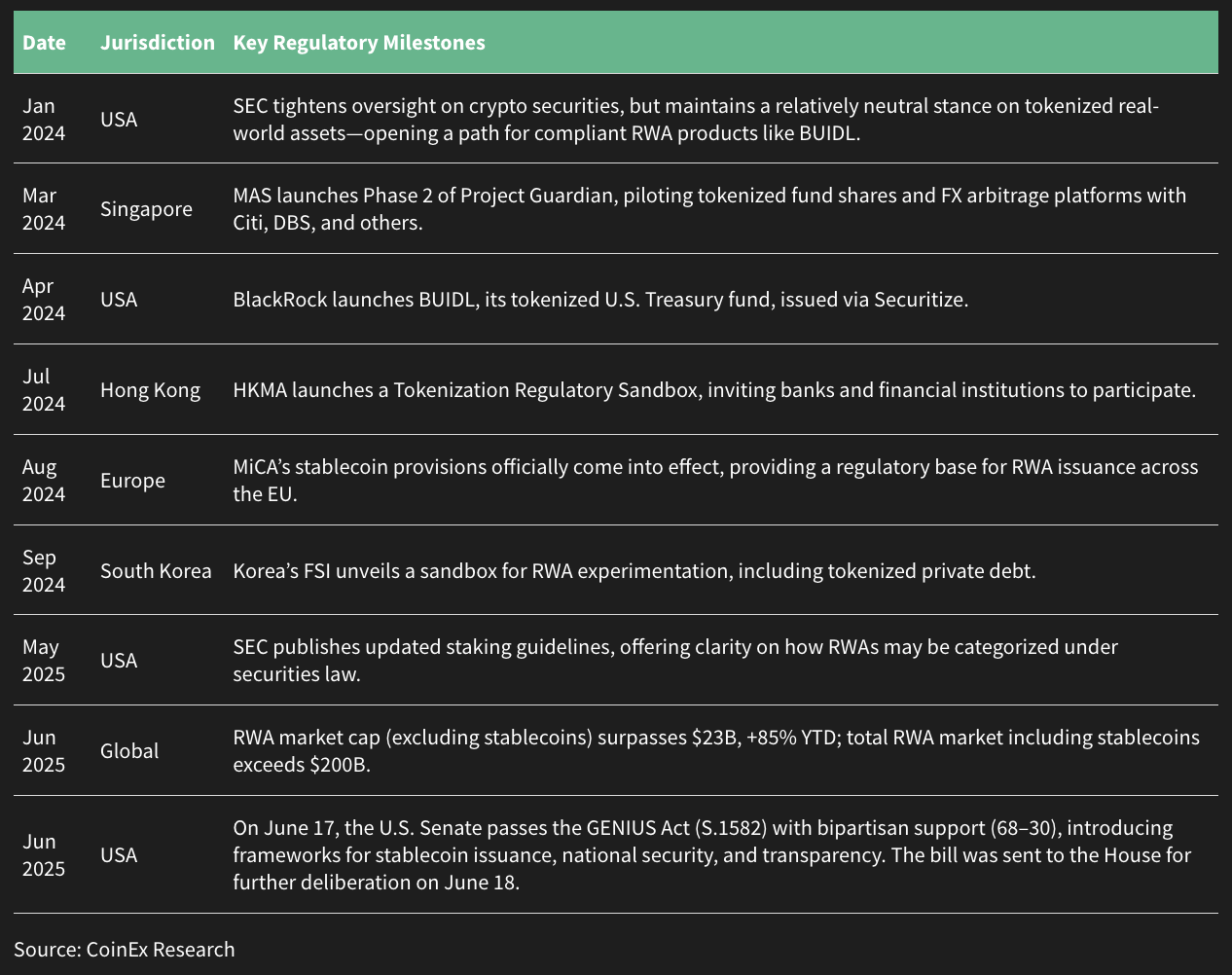

Regulatory Tailwinds: Catalyzing Institutional RWA Adoption

It was observed that regulatory clarity is rapidly transforming RWAs from experimental concepts into investable, institution-ready products. In particular, yield-bearing assets like tokenized Treasuries and private credit are benefiting most from this shift, as global regulators establish clearer compliance pathways.

Since early 2024, jurisdictions including the U.S., EU, Singapore, and Hong Kong have introduced regulatory frameworks or sandboxes tailored to tokenization. The U.S. SEC has taken a relatively permissive approach toward tokenized securities, allowing products like BlackRock’s BUIDL to launch under Reg D and Reg S exemptions. Meanwhile, Europe’s MiCA framework has gone live, establishing formal rules for stablecoins and select RWAs. Most recently, the U.S. Senate passed the GENIUS Act, further validating tokenized assets at the federal level.

Together, these developments are positioning RWAs—especially Treasuries and private credit—as the first real-world asset classes to reach institutional scale. As compliance barriers fall, capital allocation into tokenized markets is accelerating.

Challenges and Strategic Outlook

Regulatory Fragmentation and Structural Risks

While regulatory clarity is catalyzing the institutional adoption of RWAs, several structural challenges remain. These friction points will shape not only the pace of tokenization but also the design and viability of different asset classes in the coming years.

1.Regulatory Fragmentation Remains a Bottleneck

Global regulatory inconsistencies—spanning KYC, AML, securities laws, and taxation—create a complex compliance landscape. The EU’s MiCA (2025) provides a stablecoin and RWA framework, but global harmonization is lacking. In the U.S., the GENIUS Act passed the Senate but awaits full legislative approval.

2. Custodial Centralization Risks

RWA issuance, custody, and redemptions often rely on centralized entities (e.g., custodians, auditors), introducing trust and failure risks. Stablecoins and RWA funds depend on third-party attestations—any lapse in transparency can erode confidence.

3. Legal and Contractual Uncertainty

Ownership rights, enforcement, and liability for tokenized assets remain legally ambiguous. Few legal precedents exist; contracts require continuous updates by specialized legal teams.

4. Liquidity Constraints and Market Demand

Outside of stablecoins and Treasuries, most RWA categories face limited adoption and low liquidity. Institutional capital remains cautious, while crypto-native demand dominates—creating a fragmented funding landscape.

Outlook: Infrastructure First, Assets Next

Still, the direction of travel is clear. Institutional participation is accelerating—driven by familiar players like BlackRock, Goldman Sachs, and Fidelity—and a new wave of purpose-built RWA chains (e.g., Plume, Converge, Plasma) is emerging to bridge compliance with composability. Meanwhile, deeper integrations between RWA platforms and DeFi primitives (AMMs, lending markets, DAOs) are beginning to unlock real-world yield within on-chain workflows.

The foundation is now in place—but the real test lies in how well the infrastructure scales across asset types, regulatory zones, and liquidity profiles.

Conclusion: Laying the Rails for Onchain Capital Markets

The convergence of regulation, infrastructure, and institutional demand is setting the stage for RWAs to scale beyond stablecoins. However, the next phase of adoption will depend on how different asset classes evolve under varying degrees of regulation, composability, and investor appetite.

Looking ahead, the next phase—detailed in Part II—will explore how these foundational elements translate into diverse on-chain asset classes. We will analyze the tokenized markets for Treasuries, private credit, equities, sovereign bonds, and commodities, unpacking their unique regulatory challenges, design choices, and market dynamics. Together, these insights map the path for RWAs to become a cornerstone of institutional blockchain finance.

About CoinEx

Established in 2017, CoinEx is an award-winning cryptocurrency exchange designed with users in mind. Since its launch by the industry-leading mining pool ViaBTC, the platform has been one of the earliest crypto exchanges to release proof-of-reserves to protect 100% of user assets. CoinEx provides over 1400 coins, supported by professional-grade features and services, for its 10+ million users across 200+ countries and regions. CoinEx is also home to its native token, CET, incentivizing user activities while empowering its ecosystem.

To learn more about CoinEx, visit: Website | Twitter | Telegram | LinkedIn | Facebook | Instagram | YouTube

Dan Burgin

Dan Burgin