Disclaimer: The opinions expressed by our writers are their own and do not represent the views of U.Today. The financial and market information provided on U.Today is intended for informational purposes only. U.Today is not liable for any financial losses incurred while trading cryptocurrencies. Conduct your own research by contacting financial experts before making any investment decisions. We believe that all content is accurate as of the date of publication, but certain offers mentioned may no longer be available.

In January, the U.S. Securities and Exchange Commission approved the country’s first spot Bitcoin ETFs. BlackRock’s iShares Bitcoin Trust has accumulated over $17 billion in assets under management, as reported by Bloomberg, driven by significant net inflows and substantial gains in digital asset prices this year.

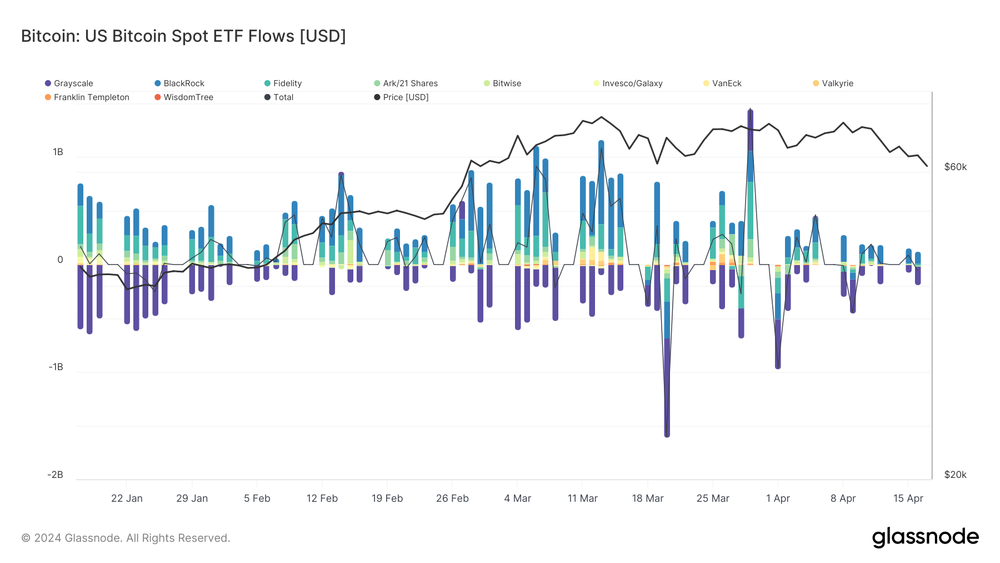

Since their launch, the 11 U.S.-based spot Bitcoin ETFs have attracted around $12 billion in total net inflows, propelling the price of Bitcoin to a record high of over $73,000 in March.

While Bitcoin ETFs experienced record-breaking inflows since January, there has been a slowdown in inflows since late March, indicating a potential shift in investor sentiment. Following substantial corrections in Bitcoin's price post-halving, significant outflows continue to occur.

Major success in beginning

Following their introduction, Bitcoin ETFs experienced robust weekly inflows ranging from $1.2 billion to $2.5 billion in the first quarter. The crypto market has experienced substantial capital flows, which in turn have strongly correlated with movements in Bitcoin prices.

Spot ETFs have created a significant source of new demand for Bitcoin, but new supply of BTC is limited to miners’ rewards. In the two-and-a-half months since spot ETFs began trading, demand from ETFs has significantly outpaced issuance.

In addition to these financial inflows, the market has also seen changes in trading patterns. For example, comparing trading volumes, spot Bitcoin ETFs now account for a substantial portion of the total spot trading volume on centralized exchanges.

As of March 31, 2024, spot Bitcoin ETFs have accumulated nearly $60 billion in assets.

Demand decreasing

BTC ETF flows started to slow due to unexpected higher U.S. inflation for the second consecutive month, compounded by the Federal Reserve's accommodative monetary policy maintaining interest rates at a 23-year high following disappointing inflation data.

The initial indication of trouble emerged on April 25 when BlackRock's Bitcoin ETF concluded its 71-day streak of consecutive inflows. During this period, IBIT saw no new inflows, with total outflows amounting to $120 million. Grayscale's GBTC also experienced significant outflows, exceeding $130 million. In contrast, Fidelity's FBTC attracted $5.6 million, and Ark's ARKB drew $4.2 million in inflows.

By May 2, every ETF recorded outflows for the first time, totaling $563.7 million — the largest losses since trading began in January. This decline has persisted for nearly two months, with funds experiencing approximately $6 billion in losses over the past four weeks, representing a 20% drop in assets under management.

Investors pulled a net $218 million from U.S. Bitcoin exchange-traded funds, one of their worst daily outflows as demand for risky investments takes a knock from fading hopes for Federal Reserve interest-rate cuts.

The significant outflows are attributed to the ongoing Bitcoin correction. Bitcoin surged by 65% from the beginning of the year to its all-time high of $73,000 in March, but has since declined by nearly 20%, currently trading close to $59,000. This decline in Bitcoin prices coincides with the onset of outflows from ETFs.

However, on May 3, Bitcoin ETFs saw the best performance in weeks. According to Farside, the Bitcoin spot ETF experienced a total net inflow of $378 million on May 3, marking the first net inflow after seven consecutive days of net outflows.

Read more on U.Today

The Grayscale Bitcoin Trust (GBTC), the largest Bitcoin ETF by assets, experienced a net inflow of new money from investors for the first time since its debut in January, with a net $63 million added to the trust.

Hong Kong did not live up

Hong Kong's spot Bitcoin and Ether ETFs made a debut on April 30. The combined trading turnover for all six ETFs reached $12.7 million. In contrast, the U.S. funds surpassed $4 billion in turnover on their first day.

Arkham Intelligence data indicates that Bosera HashKey spot Bitcoin and Ether ETFs have accumulated 964 BTC and ETH, amounting to $71.94 million in assets under management. Similarly, ChinaAMC's spot Bitcoin and Ether ETFs have amassed $123.61 million in combined assets, as reported by Eric Balchunas, a senior ETF analyst at Bloomberg.

Despite the comparatively lower asset values, Hong Kong's ETFs have garnered substantial interest. According to an April 28 survey by OSL, a Hong Kong-regulated crypto exchange, 76.9% of knowledgeable respondents in the city plan to invest in the new spot Bitcoin and Ether ETFs.

Future of Bitcoin ETFs

JP Morgan's top analyst Nikolaos Panigirtzoglou thinks that past weeks saw significant selling/profit taking in both equity and crypto markets with perhaps retail investors playing a bigger role than institutional investors.

Retail investors appear to have sold both crypto and equity funds. In terms of institutional investors, such as CTAs or other quantitative funds, they appear to have taken profit on previous extreme long positions in equities, Bitcoin and gold.

The main question is whether the demand for Bitcoin ETFs from retail investors will rebound.

Morgan Stanley reportedly expressed interest in allowing its brokers to recommend the product to their customers, but this plan was not followed by any policy yet. For now, Bitcoin spot ETF issuers currently do not have access to the clients of major registered investment advisors and broker-dealer platforms like Morgan Stanley, JPMorgan or Wells Fargo.

Significant ETF outflows often align with notable price drops in the Bitcoin market, indicating that investors tend to react to existing downturns rather than causing them. This suggests a predominantly reactive investor behavior in times of market volatility, which is crucial for understanding the causality of price movements.

Dan Burgin

Dan Burgin U.Today Editorial Team

U.Today Editorial Team