Disclaimer: The opinions expressed by our writers are their own and do not represent the views of U.Today. The financial and market information provided on U.Today is intended for informational purposes only. U.Today is not liable for any financial losses incurred while trading cryptocurrencies. Conduct your own research by contacting financial experts before making any investment decisions. We believe that all content is accurate as of the date of publication, but certain offers mentioned may no longer be available.

In a fresh post, Stellar Foundation CEO Denelle Dixon reacted to the publication of a list of digital assets that, in addition to the XLM token, also included XRP, Bitcoin, Cardano and Solana. She outlined that, for Stellar, this is not just a formality but confirmation of their strategy.

Dixon also placed special emphasis on the fact that regulatory guidance classified XLM as an example of a digital commodity. As he stated, this is something that the Stellar Foundation and the XLM community have always known since XLM was built as a public good for global payments.

Beyond Ripple rivalry: Why Stellar (XLM) being named a digital commodity is a win for RWA and Soroban

Commodity status arrived at a moment when XLM stopped being only a network for transfers and turned into a fairly powerful ecosystem. The previously launched smart contract platform Soroban has now become a major hub for tokenized real-world assets.

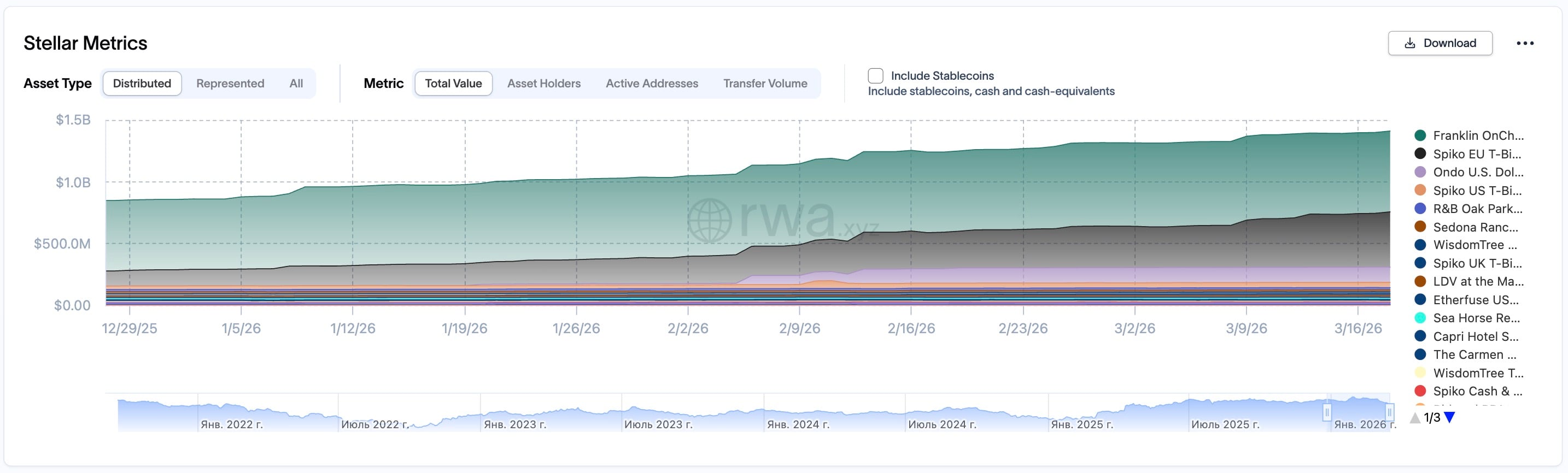

For example, according to rwa.xyz data, the distributed asset value of the Stellar network exceeds $1.4 billion. And now, when XLM is a commodity, large institutional players can further deploy their funds on Stellar without fearing regulatory claims.

Among other current breakthroughs is the fact that a money market fund from the American financial giant Franklin Templeton operates on Stellar. In addition, there is a non-U.S. government debt fund focused on European treasuries, Spiko EU T-Bills Money Market Fund, worth $447 million.

For a long time, XRP was considered the only legal payment asset in the United States after the Ripple vs. SEC court case. Now this advantage is gone. Since March 17, both assets have identical Digital Commodity status. One can conditionally divide their positioning in such a way that while XRP focuses on banking liquidity, XLM is moving into the DeFi sector and asset tokenization through more flexible smart contracts.

Moreover, as oversight shifts toward the CFTC, a wave of applications for a Stellar ETF can be expected, and it would be surprising if they do not appear on the market by the end of the year.

U.Today Editorial Team

U.Today Editorial Team Dan Burgin

Dan Burgin